Introduction

Creating a saving money budget plan that fits real life expenses is essential for anyone who wants to take control of their finances. It helps you understand where your money goes and how to allocate it wisely. Many people find budgeting hard because life expenses can be unpredictable, but a smart budget adapts to your actual spending habits.

This article explores simple and practical ways to build a budget that matches your daily life. You will learn how to plan your income and expenses, reduce unnecessary spending, and save money without feeling deprived. The goal is to help you build a budget that supports your lifestyle while enabling you to save for future goals.

Why Budgeting Matters for Saving Money

Budgeting is more than just numbers on paper. It’s about taking control of your money instead of letting it slip through your fingers. When you have a budget, you see clearly where your money comes from and where it goes. This clarity often sparks small but powerful changes in everyday spending habits. For example, you might realize you’re spending more on takeout than you thought, or that skipping a gym membership could free up cash for savings.

Without a budget, it’s easy to overspend without meaning to. You might think you’re managing fine until a bill arrives or your bank balance surprises you in a not-so-good way. Budgeting helps prevent this by setting boundaries on spending.

On a day-to-day level, a budget can reduce money stress. It’s like having a map that shows you what’s safe to spend and what to save. When you budget, saving money feels less like a chore and more like a natural part of what you do each month.

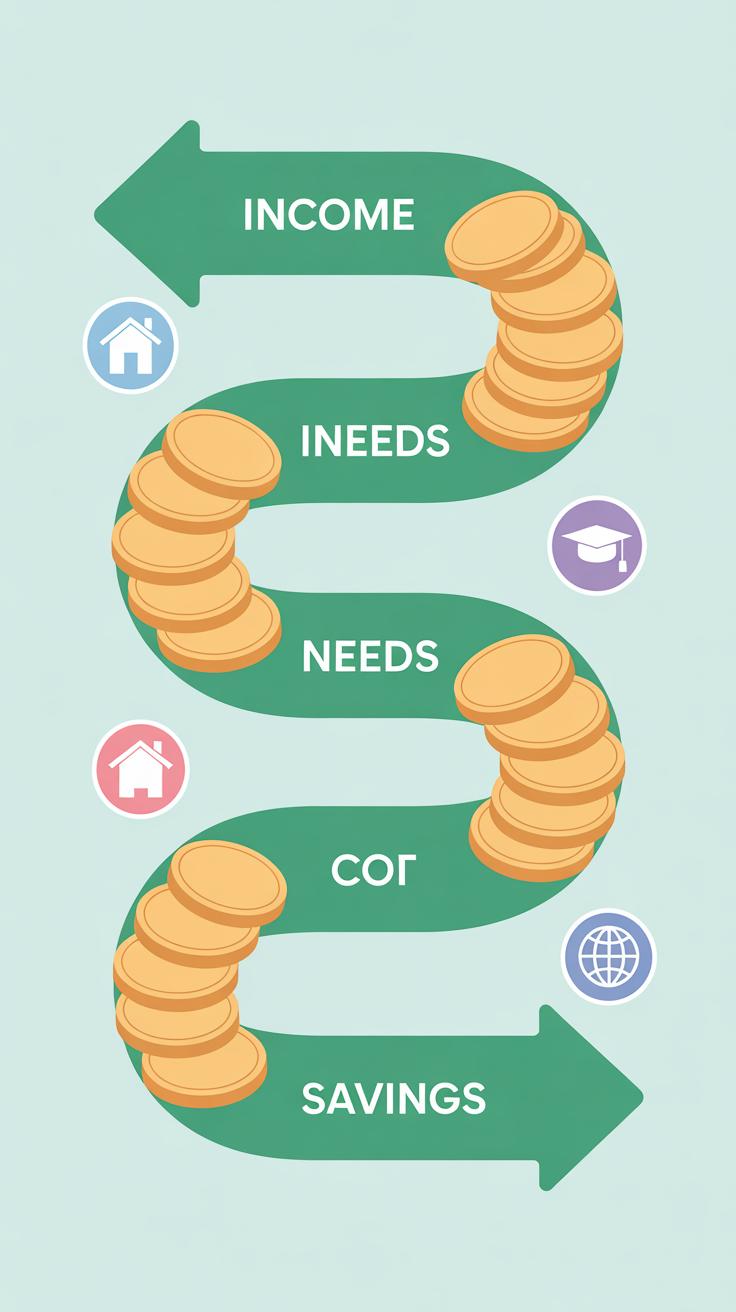

A budget is simply a plan for your money. It lists where your income comes from, what expenses you have, and what part you want to save. Creating one starts with figuring out how much money you bring in — from your job, side gigs, or any other source.

Next, you write down your expenses. Some are fixed, like rent or a car payment. Others vary, like groceries or entertainment. Don’t worry if this takes a few tries to get right. You’ll learn and adjust as you go. The goal is to know roughly how much you spend in each category.

Finally, you decide how much to set aside as savings. This can be as little or as much as you’re comfortable with. Even small amounts add up over time. The main point is to include savings as a fixed “expense” in your budget — treating it like a bill that must be paid.

When you budget, you control what you spend rather than just reacting to impulses or emergencies. You might discover, for example, that your streaming services add up to more than you thought, so you can choose to cancel a few.

This control is key because it prevents waste and helps you prioritize saving. Instead of wondering where your money went at the end of the month, you decide in advance. That’s a big shift.

It’s hard to save if you have no clear picture of your spending. Budgeting lets you see the patterns and make smarter choices. Over time, this control builds habits that make saving easier and more consistent, which is often the hardest part.

Track Your Income and Expenses Accurately

Getting a handle on your money starts with knowing exactly how much you bring in and how much you’re actually spending. It’s not enough to estimate or rely on memory—it’s about carefully tracking every dollar. You might think you know what’s going out, but small daily expenses can sneak in unnoticed. Over time, those small costs add up, and your budget loses its accuracy.

First, list all your sources of income. Don’t just stop at your main salary. Include freelance work, side gigs, dividends, or any occasional earnings. For example, if you pick up some extra hours on the weekend or sell items online, they count too. Sometimes people forget these extras because they aren’t regular, but they do impact your overall cash flow.

Next, record every expense. Yes, it feels tedious to track that morning coffee or spontaneous snack purchase, but these little things shape where your money really goes. Try using apps like Mint or YNAB (You Need A Budget), or even a simple spreadsheet if you prefer. Some find writing expenses in a small notebook more direct. Pick what fits you and stick with it.

Most importantly, review your tracked data weekly. Seeing patterns emerge helps you adjust spending habits before the month ends. Maybe your “just this once” purchases happen more often than you thought. Tracking puts you face to face with your real habits—and lets you decide what to change.

Set Realistic Budget Goals Based on Your Life

When setting budget goals, you want them to fit your real life—not some ideal version of it. That means looking closely at your actual expenses and lifestyle. For example, if you take public transport daily, your transportation cost is fixed, but if you rarely eat out, then budgeting a big allowance for dining might not be realistic.

Try to keep your goals achievable. If you’ve never saved before, aiming for 50% of your income might be unrealistic. Instead, start small—maybe 5 or 10%. You can always adjust as you go. Flexibility is key because life throws curveballs—unexpected bills, or maybe you want to try a hobby that costs money.

Balancing needs and wants can be tricky. Needs are essentials like housing, food, and utilities—things to cover first. Wants, like that new gadget or extra streaming service, come after. Prioritize spending by focusing more on needs to keep stable, then gradually add some wants so you don’t feel deprived.

And don’t forget to leave some breathing room in your budget. Unexpected expenses will come up. Maybe your car needs repair, or a friend invites you out unexpectedly. Also, budgeting a small amount for fun is not a waste—it keeps motivation high and helps avoid burnout. It might feel counterintuitive, but budgeting isn’t about cutting out everything enjoyable. It’s about balance.

Identify and Cut Unnecessary Expenses

Spotting expenses that quietly drain your budget isn’t always easy. Some costs sneak in under the radar because they seem small or routine. But over time, they add up and eat into your potential savings. Think about those monthly subscriptions you barely use—or maybe you forgot you even signed up for. It happens to a lot of us.

Common unnecessary expenses often include:

- Unused or rarely used streaming services and apps

- Frequent eating out or takeout meals

- Impulse purchases during casual shopping trips

- Overpriced convenience items, like bottled water or single-use coffee

- Extra data or mobile plan features you don’t actually need

You might assume small things don’t matter much, but skipping a few takeout lunches or dropping one subscription could free up a surprising amount each month. It’s worth asking yourself—do I really get value from this?

Cutting back is tricky though. Sometimes we keep subscriptions “just in case,” or grab a coffee out because it feels easier. If you want practical steps, start by reviewing your bank statement carefully, line by line. Cancel anything that doesn’t spark a clear benefit. Set a rule for eating out, maybe once a week maximum. And try delaying impulse buys for 24 hours—often the urge fades.

It requires honesty and a bit of patience. But the more unnecessary expenses you identify and trim, the more room you make for actual saving rather than just spending less miserably. It’s about choices—you don’t have to give up everything, just focus on what really matters to you.

Use Budgeting Tools and Technology

Keeping a close eye on your spending isn’t easy. There’s a lot going on daily, and it’s tempting to just forget about it until the end of the month—which can lead to surprises. That’s where budgeting tools come in. They help take some of the guesswork away by tracking expenses automatically—so you don’t have to remember every little coffee or impulse buy.

Apps That Simplify Budgeting

Some apps really make life simpler. For example:

- Mint: Connects to your bank accounts to track your spending and categorize expenses. It sends alerts when you’re close to overspending in a category.

- YNAB (You Need A Budget): Focuses on assigning every dollar a job. It might feel a bit strict, but it helps many people stick to budgets more seriously.

- PocketGuard: This one shows how much “spendable” money you have after bills and goals. It cuts through the clutter when you just want to know what you can actually use.

These apps can feel like having a personal finance assistant—except they don’t drink your coffee or judge your spending habits. They keep running in the background and help you catch where your money’s really going.

Manual vs Digital Budgeting

Now, some people swear by pen and paper. There’s something satisfying about writing down your budget, seeing it in front of you. It forces you to slow down, maybe notice details you’d miss otherwise.

But manual budgeting means more work. You have to update it yourself, remember to record expenses, and double-check your math. Digital tools automate all that. They’re generally faster and less prone to errors—except when syncing fails or categorization is off.

Writing by hand can feel personal and reflective, which helps some folks stay engaged. On the flip side, apps give instant insights and charts that make trends easier to spot.

So maybe the choice depends on your style. Would you rather build a habit through action and reflection, or do you prefer convenience and data at a glance? Both have their place—sometimes I find myself switching between the two, depending on what stage my finances are at.

Plan for Short Term and Long Term Savings

When thinking about saving money, it’s easy to focus on just one goal—like a vacation or an emergency—but splitting your savings between near-term and long-term needs makes more sense. You want some cash ready for the stuff that might pop up soon, say a car repair or a small home upgrade, while also setting aside funds for bigger things farther down the road.

It doesn’t have to be complicated. Consider dividing your savings this way:

- Short-term: Money you can access within a year or two, for immediate plans or unexpected costs.

- Long-term: Funds locked in for things like retirement or a child’s college tuition, where growth over time really matters.

It may feel tricky at first, especially if your income fluctuates, but even a small percentage monthly—like 10% to short-term and 5% to long-term—can build up over time. Over time—I suspect you’ll find the balance that feels right for your life, even if that balance shifts now and then.

Emergency Fund Basics

An emergency fund is the backbone of short-term savings. Think of it as a safety net for those times when life throws curveballs: job loss, unexpected medical bills, urgent car repairs. Without it, you might have to rely on credit cards or loans that drag you down with interest.

Here’s what works when building one:

- Start small. Even $500 can cover minor emergencies at first.

- Aim for three to six months’ worth of essential expenses.

- Keep it in a separate, easily accessible account so you’re not tempted to tap in for non-emergencies.

Building the fund might feel slow, but it’s about consistent contributions—weekly or monthly. Think about it like a safety measure you just can’t afford to skip.

Saving for Dreams and Retirement

Beyond the emergency fund, there’s saving for the goals that pull you forward: a college education, a dream trip, or retirement. These often require a different approach because they’re usually years away and involve larger sums.

Try weighting your savings toward investments or accounts that offer growth potential. For example, retirement accounts or education savings plans may have tax perks. But also keep a sense of flexibility—life changes, and sometimes goals evolve faster than expected.

Planning might mean setting smaller milestones that add up—a few hundred dollars a month for travel funds or putting a percentage of your raise each year into your retirement fund. It’s not just about squirreling away money; it’s about making those dreams real in a manageable way.

Make Adjustments When Life Changes

Your budget is not some fixed thing you set once and forget. Life happens—new job, growing family, unexpected bills—and your budget needs to reflect that. If you keep using the same spending plan despite big changes, you might find yourself either stressed or ignoring your budget altogether. That’s why revisiting your budget regularly isn’t just helpful, it’s necessary.

Recognizing When to Change Your Budget

How do you know your budget is out of sync? Look for signs like:

- You’re consistently overspending in certain categories, making other parts of your budget hard to balance.

- You suddenly have new income or expenses—like a raise, switch to freelance work, or caring for a new family member.

- You feel anxious or guilty about your spending habits—maybe because things feel tighter than before or savings aren’t growing.

- Your financial goals have shifted, maybe moving from saving for vacation to paying down debt.

If any of this sounds familiar, consider it a nudge that your budget needs attention.

Steps to Update Your Budget

Updating your budget doesn’t need to be complicated. I usually start by listing all new income sources and expenses, then compare them against my old budget.

Next, I prioritize what really matters now. For example, after switching jobs, my commute costs changed, so I moved some funds from transportation to emergency savings, just in case. Then, look for flexible areas—subscriptions you no longer use or dining out habits that can be trimmed.

From there, reallocate your money thoughtfully. Adjust spending limits, update savings targets, and try to be honest with yourself about what’s realistic—not perfect. Finally, keep monitoring how these changes stick. It’s okay to tweak again as life throws its next curveball.

Does your current budget reflect the life you live today, or the life you had last year? It’s okay to admit it might be time for a tune-up.

Stay Motivated to Stick with Your Budget

Keeping your budget going over time can feel like a slow uphill climb. It’s easy to start strong but then lose steam. One way to stay on track is by celebrating the small wins. Maybe you managed to cut back on dining out this week or paid off a bit more on a credit card than usual. Recognizing these little victories, even if they seem minor, can build momentum. I found that jotting down a quick note or marking progress on a calendar helped me feel like I was moving forward. It’s a reminder that your effort isn’t invisible.

Setbacks happen—

perhaps you overspend one week because an unexpected bill popped up or stress led you to impulse buys. Instead of beating yourself up, try viewing these moments as part of the process, not failures. Ask yourself: what triggered the slip, and how can I adjust? Sometimes, just acknowledging what went wrong brings clarity and helps you reset without guilt.

- Celebrate progress by tracking small achievements regularly.

- Use tangible reminders like notes or charts to visualize success.

- When spending derails, reflect on the cause rather than focusing solely on the mistake.

- Be kind to yourself—budgeting isn’t a straight line.

- Adjust your plan as needed without feeling like you’ve given up.

Staying motivated isn’t about perfect discipline. It’s about finding a rhythm that keeps you feeling capable, even when things go sideways.

Avoid Common Budgeting Mistakes

Ignoring Small Expenses

You might think a few dollars here and there don’t matter much. Maybe that daily coffee, a snack, or a quick app purchase seems insignificant. But these small expenses add up, more than you’d expect. Ignoring them can quietly drain your budget without you realizing it, leaving you scratching your head at month-end, wondering where your money went.

Tracking these minor spends doesn’t have to be a hassle. Try keeping a note on your phone or use a simple app. You don’t have to obsess over every penny, but being aware changes how you spend. I remember once ignoring my small takeout snacks; only when I tracked them did I see they accounted for nearly 10% of my monthly spending. That was a surprise. So, ask yourself: have you checked how those “small” expenses affect your finances lately?

Setting Unrealistic Budgets

Creating a budget that’s too tight or too idealistic sets you up for frustration. I mean, if you budget for zero fun or ignore the unpredictability of life, chances are you’ll abandon your plan soon. It’s tempting to aim for big savings right away, but if your budget can’t flex a little, it becomes almost impossible to maintain.

Realistic budgets reflect your actual spending habits and priorities. Instead of pinching every penny, try building in small allowances for treats or unexpected costs. Think about your lifestyle – does your budget feel sustainable for a few months? You don’t want it to be so loose that it’s meaningless, but, well, it shouldn’t feel like punishment either. What balance are you aiming for?

Build Healthy Money Habits for Life

Creating lasting habits around your budget isn’t about being perfect every day. It’s more about consistency over time, even when things feel messy or unpredictable. One good practice is to schedule regular money check-ups. Maybe once a week or every two weeks, take a moment—just a few minutes—to review what you’ve spent and saved. This small habit helps keep you grounded and prevents surprises from sneaking up. I’ve noticed that when I skip those check-ins, it’s easier to let careless purchases pile up without realizing.

Planning ahead goes hand in hand with these reviews. Think beyond next week or even next month. What expenses could be coming down the line? Perhaps a car maintenance, seasonal utility bills, or a gift for someone’s birthday. Writing these down and factoring them into your budget gives you breathing room and peace of mind. You don’t have to plan every single detail, but sketching out probable costs helps you avoid last-minute scrambles.

Try setting reminders for these money check-ups. Over time, they’ll feel less like chores and more like natural pauses. The more you anticipate future expenses, the less money stress tends to creep in. It’s almost like building a muscle: the more you use it, the stronger and more automatic these habits become. Even if you stumble or forget once in a while, keep going. Habits aren’t built in a straight line, after all.

Conclusions

Building a saving money budget plan suited to your real life expenses takes practice and attention. By tracking where your money goes and making informed choices, you can balance your spending and saving effectively. Budgeting is not about strict limits but about making your money work for you.

Remember, small consistent changes add up. Keep adjusting your budget as your life changes and celebrate your progress. The steps in this article can help you create a budget plan that keeps you in control and helps you save for the things that matter to you.