Introduction

Budget planning is a basic skill everyone should learn. It means making a plan to manage your money, especially how you spend and save what you earn. For beginners, it might seem tricky but with simple steps, anyone can create a budget that helps keep money matters clear.

This article explains how to build a budget using your paycheck wisely. You will learn how to divide your earnings to cover needs, wants, and savings. The paycheck strategy makes it easier to control your money so you avoid running out before the next paycheck arrives.

What is Budget Planning

Budget planning means making a simple plan for your money. It helps you see how much money comes in and how much goes out. The main goal is to balance these two—your income and your expenses—so you don’t spend more than you earn. Think of it as a way to keep control of your money instead of letting money control you.

When you plan your budget, you think about what money you have, like a paycheck, and what money you need to pay, like bills or groceries. You try to make sure you have enough money for the things you need without running out before your next paycheck. This helps you avoid stress and surprises when money feels tight.

Budget planning includes a few key parts, but mostly it’s about paying attention to your income, tracking your expenses, and figuring out how much you can save. It sounds simple, but it can really change how you manage your money every day.

Why Budget Planning Matters

Why does budget planning even matter? Well, imagine having a few dollars left and then suddenly an unexpected bill shows up. If you didn’t plan, that could be a big problem. Budgeting helps you avoid that situation. It also means you can save for special things—maybe a new phone or a trip. That feels pretty good, knowing you have money set aside for stuff you really want.

Thinking about your own money, do you know where most of it goes? Do you ever feel like you spend without noticing? Budget planning can help answer these questions and create better habits.

Also, life likes to throw surprises. What if your phone breaks or you need to visit a doctor? Having a budget helps you be ready instead of scrambling to find money. It might seem a bit strict, but it actually gives you freedom when unexpected things happen.

Key Parts of a Budget

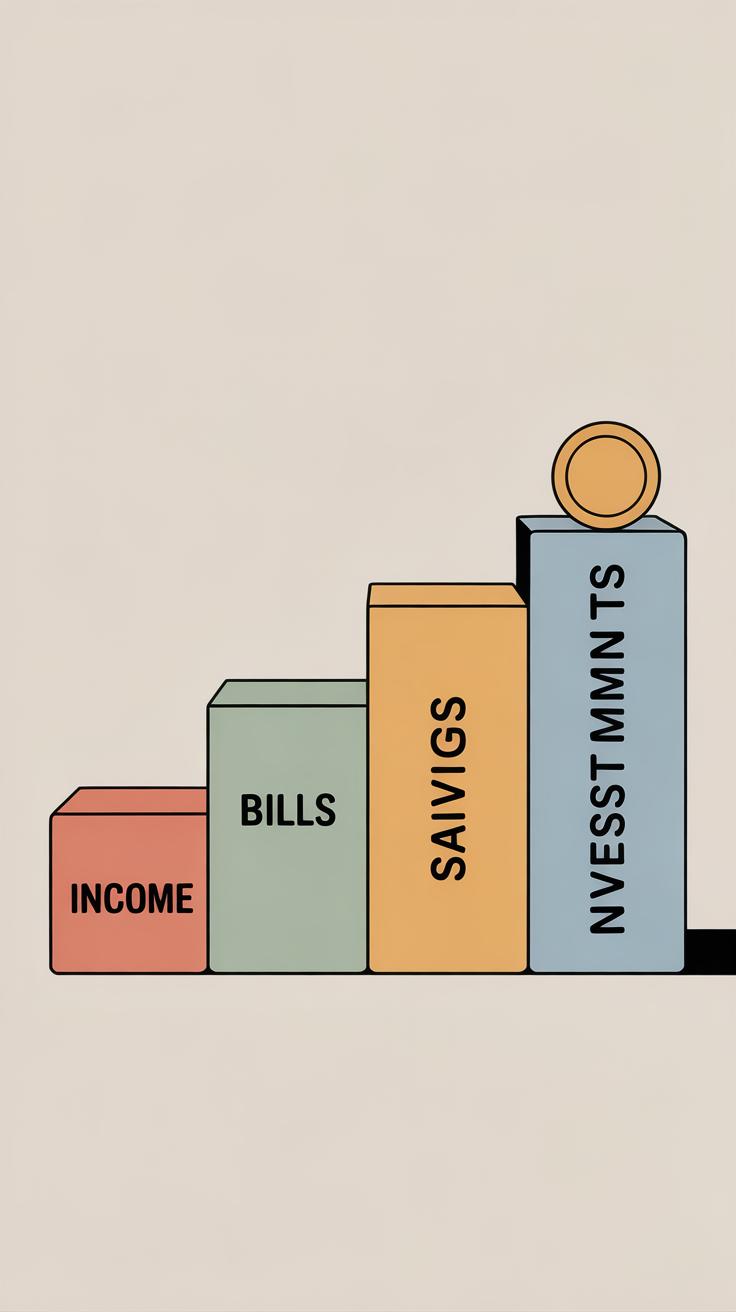

Every budget has three main parts: income, expenses, and savings. Let’s break these down simply.

- Income: This is the money you get, often from your paycheck. Think of it as the money you bring home.

- Expenses: These are the things you have to pay for, like rent, food, electric bills, or even your phone plan.

- Savings: This is the money you set aside for future use, maybe for emergencies or something special you want.

When you plan your budget, you write down how much money you expect to receive and then list out what you’ll spend. The leftover money after expenses is what you can save. If this sounds tricky, it really isn’t once you start paying attention to where your money goes.

How to Calculate Your Income

Understanding Paychecks

Your paycheck is more than just a piece of paper or a direct deposit notice. It’s a snapshot of the money you’ve earned—and more importantly, what you actually get to keep. Each paycheck shows your total pay before anything is taken out, known as your gross income. But the number you probably care about most is what lands in your bank account after taxes and deductions. That’s called your net income. Knowing this amount feels necessary if you want to budget, but it’s easy to overlook or misunderstand what’s on your paycheck.

On the paycheck, you’ll usually find a few key things:

- Gross income: the total money you earned before anything is taken out.

- Taxes and deductions: money taken out for things like federal and state taxes, Social Security, and sometimes insurance or retirement contributions.

- Net income: what you actually take home, after all those deductions.

Finding Your Net Income

Figuring out your net income is a practical step in budgeting. Say your gross income is $1,000 for a two-week pay period. From that, taxes and deductions might take away about $200, leaving you with $800 to use. This $800 is your net income.

You can check your paycheck or pay stub for exact amounts taken out. Sometimes it’s confusing because there are multiple tax lines, but the total deductions are usually listed. Add those up and subtract them from your gross income.

Knowing your net income helps you plan realistically. After all, budgeting based on the gross income is like building a house on shaky ground. Would you want to imagine you have more money than you really do? Probably not.

So, when you look at your paycheck next time, try this little exercise: read the gross pay, note the deductions, subtract, and see what’s left. This number is your baseline—the real money you have to work with.

Tracking Your Expenses

To really understand where your money goes, you need to track everything you spend. This means jotting down every purchase, no matter how small or seemingly insignificant. A coffee bought on a rushed morning, a snack from the vending machine, bus fare for your daily commute, or even utility bills—they all count. When you look away, these small expenses quietly add up.

Why does this matter? Because without tracking, you might think your spending is under control, but surprise! Those small, repeated costs can throw your budget off balance. For example, you might feel like your money vanishes despite paying rent and groceries on time. Tracking every penny—really every penny—can reveal surprises and patterns.

You don’t need fancy tools. A simple notebook works fine if you prefer writing by hand. You might find a phone app handy, especially if you’re on the go and can log expenses instantly. Or, if you like numbers and charts, a spreadsheet can help you organize expenses by type and date. The key is consistency.

When you keep a clear record, you start noticing habits. You can decide which expenses are necessary and which could be cut down, or at least adjusted. Tracking your spending isn’t just about controlling money; it’s about understanding your financial habits better. And if you’re anything like me, sometimes just seeing the numbers laid out feels like a reality check. So, why not give it a try for a week or a month? You might be surprised by what you learn.

Creating Budget Categories

When you look at your expenses, grouping them makes managing money less confusing. Splitting your spending into three categories—needs, wants, and savings—helps you see where your money goes and where it should go.

Needs are things you must have. They keep you safe, healthy, and able to function daily. Think of food, rent, or electricity bills. If you skip these, life gets tricky fast.

Wants are nice to have but not essential. Buying a new video game, eating out, or a fancy coffee falls here. They add comfort or fun, but you can cut back on them when money is tight.

Savings set aside money for goals or emergencies. This might be saving up for a bike or putting cash away in case something unexpected happens. It’s the money you don’t spend now but plan to use later.

Sorting expenses this way isn’t perfect—it can feel awkward sometimes to decide if something is a need or want. Like, what about phone plans? Some consider even the simplest phone a need. Your view might shift depending on your life.

What Are Needs and Wants

Understanding the difference between needs and wants can be trickier than it sounds. Needs keep you alive and well—things you truly can’t skip. Wants, meanwhile, are extras you don’t need immediately. For example:

- Needs: groceries, shelter, basic clothes

- Wants: a new pair of sneakers, streaming service, dining out

Sometimes, these blur. A laptop might be a need if you use it for work, but just a want if it’s only for gaming. Thinking this way might change how you spend.

Setting Savings Goals

Saving money isn’t just about putting cash away; it’s about giving yourself choices. When you save, you build a little buffer against surprises or can buy something special later.

Start simple. Maybe you want a toy or a small trip. Or, save for an emergency, like a sudden bike repair or school supplies. Set a target and a time frame—say, $50 in three months—and put a bit aside regularly.

It can feel slow at first, and you might wonder if it’s worth it. But watching your savings grow, bit by bit, can be surprisingly motivating. What do you want to save for now?

Making a Paycheck Strategy

When your paycheck arrives, it’s tempting to just spend whatever feels right at the moment. But what if you could make your money last longer and work harder by splitting it up immediately? Dividing your paycheck as soon as you get it—whether by using envelopes, separate bank accounts, or budgeting apps—can really help you stay on track.

Try this simple division:

- Needs: Rent, groceries, bills—things you absolutely must cover.

- Wants: Coffee, dining out, small treats—things that add pleasure but aren’t essential.

- Savings: Emergency funds, retirement, or future goals.

Putting the money into these categories right away means you see exactly what you have for each, reducing the chance of overspending. It’s like setting boundaries early.

Sticking to those divisions can be tougher. Imagine you’re eyeing an extra pastry at the bakery. Your “wants” envelope only has so much, so you might have to pass it up or wait until next payday. This little discipline feels awkward at first but builds up over time.

Sometimes you might even hesitate to dig into your savings for just one night out. That pause is exactly what helps you prioritize and avoid regrets later. Of course, life throws curveballs and plans change—but making this split from day one gives you a clearer path, even if you don’t stick to it perfectly every time.

Adjusting Your Budget When Needed

Life rarely sticks to a plan, and your budget shouldn’t either. It’s a good idea to check in on your budget regularly—say, monthly or whenever something big changes. Maybe your rent goes up, or you get a freelance gig that boosts your income. Either way, you’ll want to tweak your numbers so your budget works with your reality, not against it.

When expenses rise, think about where you can cut back. Could you pause a streaming service or pack lunch a bit more often? Moving some money around is okay—you might shift funds from entertainment to essentials for a while. Unexpected costs happen, and adjusting early can stop stress from piling up. Try to stay calm about it; budgeting isn’t about being perfect, but staying flexible.

If your income increases, try to boost savings. That might mean skipping a few non-urgent purchases or putting any overtime money into a savings jar—literally or digitally. Sometimes extra work or selling unused items can add a bit more cushion. It’s tempting to spend more when you earn more, but saving first usually feels better in the long run, even if it’s just a little at a time.

Do you find reviewing your budget overwhelming? Breaking it into steps can help: review income changes, list new or raised expenses, then decide what to cut or save. Your budget is a tool, not a burden. Make changes often enough to keep it useful, but not so often that it feels like a chore.

Avoiding Common Budget Mistakes

One of the trickiest things about budgeting is missing those small expenses that slip through the cracks. You might think a couple of coffee runs or spontaneous app purchases don’t matter much. But over weeks or months, they add up—sometimes enough to throw off your entire plan. So, it’s not just about the big bills; you need to track little costs too, like parking fees or those occasional snacks. It might feel tedious, but writing them down or using a simple tracking method keeps your budget closer to reality.

Overspending on wants is another common snag. It’s easy to confuse a want with a need, especially when sales or promotions pop up. Saying no isn’t easy, and you might find yourself justifying a purchase “this once.” But regularly resisting these impulses can grow your savings more than you expect. Try setting monthly limits for non-essentials or pause before buying—ask yourself if you really need it now or if it can wait.

By catching those small expenses and keeping non-essentials in check, you’ll keep your budget honest. Have you noticed subtle leaks in your spending before? Maybe this is what’s been holding your budget back. Try pausing to reflect on these habits; they might surprise you.

Using Tools to Help Budgeting

When it comes to managing your money, having the right tools can make a real difference. Maybe you’ve tried keeping track in your head or on random notes, but things get messy fast. That’s why budget apps, spreadsheets, and even good old envelopes can help keep your finances more organized and visible.

Spreadsheets, for example, are flexible and let you tailor everything exactly how you want, which is great if you like control. But they do take some patience to set up and update regularly. On the other hand, budget apps automate much of the tracking, giving you updates right after you spend or get paid — almost like having a money coach in your pocket.

Envelopes might sound a little old-fashioned, but dividing cash into labeled envelopes—for groceries, bills, entertainment—can really make spending limits tangible. Some people find it easier to stick to budgets when they actually see the money leaving those envelopes.

Simple Budget Templates

If you’re new to budgeting, starting with a simple template can feel less overwhelming. A basic sheet that lists your income sources and categories of spending—housing, food, transport, savings, and so on—is a good start. It doesn’t need to be fancy. Even jotting this down on paper works. For example:

- Income: paycheck, any side jobs

- Fixed expenses: rent, utilities

- Variable expenses: groceries, gas

- Savings goals

Writing it out like this gives you a clearer view of where your money is going. And don’t worry if your numbers don’t add up perfectly at first. Budgets are often a work in progress.

Apps to Make Budgeting Easy

Apps can automate much of this for you, which sometimes feels like magic. A few beginner-friendly options include Mint, EveryDollar, and Goodbudget. These let you connect your bank accounts, then track paycheck deposits and spending automatically.

You don’t have to be tech-savvy to use them. The interfaces are usually pretty simple, and they help you spot patterns you might otherwise miss. For example, you might see you’re spending more on takeout than you thought, or forget a small recurring subscription that adds up over time.

So, have you tried using any tools yet? Sometimes, it’s about finding what fits your style. Maybe a spreadsheet keeps you engaged, or maybe an app takes the burden off your shoulders. Either way, tools can help you stay on top of your money without feeling overwhelmed.

Planning for Big Expenses

Big expenses, like a school trip, presents for birthdays, or new clothes for the season, can quickly throw your budget off track if you don’t prepare. Saving for these costs feels less daunting when you start early—maybe even months ahead. Imagine a school trip that costs $300. Instead of stressing last minute, you could set aside $50 from each paycheck over six paychecks. Breaking things down this way makes it manageable.

Here’s a way to think about it:

- Pick the total amount you need.

- Count how many paychecks you have before the expense.

- Divide the total by that number to find the amount to save each time.

That approach spreads out the effort, so you’re not scrambling or tempted to borrow money.

Next, ask yourself: “Which big expenses can I realistically cover first?” Maybe the school trip is non-negotiable this year, but new clothes could wait. Prioritize what feels more urgent or important to you. Personal events, like birthdays or holidays, might also need a budget slot early on. Of course, your priorities might shift unexpectedly. That’s okay. Just keep adjusting your plan until it fits your situation better.

Building Good Money Habits

Budgeting isn’t just a one-time task—it’s something you want to practice regularly. Watching your spending closely helps you catch patterns you might not notice otherwise. Maybe you’ll spot that small daily coffee or those unexpected online purchases creeping up. Saving regularly, even if it’s just a small amount, builds momentum. It’s surprising how those little contributions add up over time.

Reviewing your budget each month gives you a chance to adjust what’s not working. Sometimes expenses change, or maybe you realize you overestimated how much to set aside for certain things. Taking this time keeps your plan fresh and realistic.

Make Budgeting a Routine

Try simple habits like checking your spending journal a few times a week—nothing too overwhelming, just enough to stay aware. Mark down expenses, compare them with your budget, and think about what you might do differently. This kind of regular focus can help avoid surprises when month-end comes. You might feel a bit impatient at first, but it really settles into a good routine after a while.

Celebrate Your Progress

Don’t overlook the power of rewarding yourself. Meeting savings goals or sticking to your plan isn’t always easy. When you succeed, acknowledge it. Maybe treat yourself to something small but meaningful—a favorite snack, a movie night, or a little outing. These moments keep motivation alive and make budgeting less like a chore. After all, you’re working for your future and that deserves some recognition.

Conclusions

Budget planning using the paycheck strategy keeps your money organized. By creating clear categories for your spending and savings, you avoid stress and surprise debts. The process helps you see where your money goes and helps you plan for needs and future goals.

Starting a budget is simple and valuable. Use your paycheck as the base for your plan. Track your spending carefully and adjust your budget to fit your life. You will gain confidence managing your money and reach your goals step by step.